Part I of Timber REITs and the “Dividend Tax” Cliff summarized, in words, the implications to shareholders of publicly-traded timberland-owning REITs if the current dividend tax rate expires on December 31, 2012. This post quantifies the implications and puts into context the impact of changing tax rates on timber REIT shareholders relative to shareholders of non-timber REITS or other dividend-paying stocks in the United States. The bottom line: timber REIT equities retain a tax-advantaged status in a post-tax cliff environment.

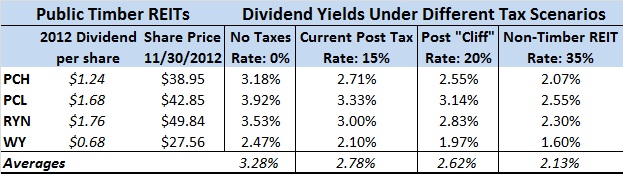

Let’s compare the dividend yields of the four public timber REITs – Potlatch (PCH); Plum Creek (PCL); Rayonier (RYN); and Weyerhaeuser (WY) – under different assumed tax scenarios:

- No Taxes: our “fantasy” and “frictionless plane” scenario.

- Current Post Tax: reflects the present code that taxes dividends at 15%.

- Post “Cliff”: represents a return to pre-2003 rates, which treats timber REIT dividends as (mostly) capital gains and taxes them at the pre-2003 capital gains rate of 20%.

- Non-Timber REIT: captures a return to taxing dividends at the marginal ordinary income tax rate. Our scenario focuses on shareholders in the 35% ordinary income tax bracket.

Table 1 summarizes how the impact on dividend yields, while negative in all scenarios, slices results to a greater degree for non-timber REITs.

Table 1

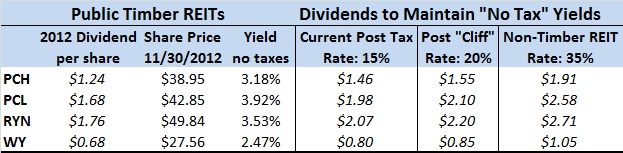

What would you need to receive in dividends from your timber REIT investments to generate the same dividend yield “pre” versus “post” change in the tax code, if it occurs? Table 2 summarizes this result relative to non-timber REIT shares.

Table 2

While dividend yields do not tell the whole story, they do provide a starting point for comparing alternate investments. At a minimum, stocks that emphasize dividends compete with risk-free rates offered by U.S. Treasuries (currently 1.63% pre-tax for 10 years). Other factors to consider include:

- Total expected returns: investors reasonably expect a risk “premium” for holding stocks over bonds, and this premium supports expectations of total returns which sum dividends and appreciation.

- Effective tax rates: actual tax rates vary significantly across investors. Institutions such as mutual funds and pension funds hold approximately two-thirds of public equities in the U.S. And many individuals attracted to dividend-paying stocks pay lower ordinary income tax rates.

In the end, regardless the valuation math and legislative decisions, timber REITs, in the world of dividend-paying stocks, feature an attractive tax profile for potential investors.

Click here to learn about and register for “Applied Forest Finance” on February 7th in Atlanta, Georgia. The course details necessary skills and common errors associated with the financial and risk analysis of timberland and other forestry-related investments.

Leave a Reply