This is the third in a series related to timberland investments. Previous posts addressed benchmarking private timberland investments and the valuation of timber REITs.

How have private timberland investments performed relative to other asset classes? This question opens the door to a series of follow-ups such as:

“Over what time frames?”

“Relative to which other asset classes?”

“Based on whose benchmarks and what investment objectives?”

“Using what data sets?”

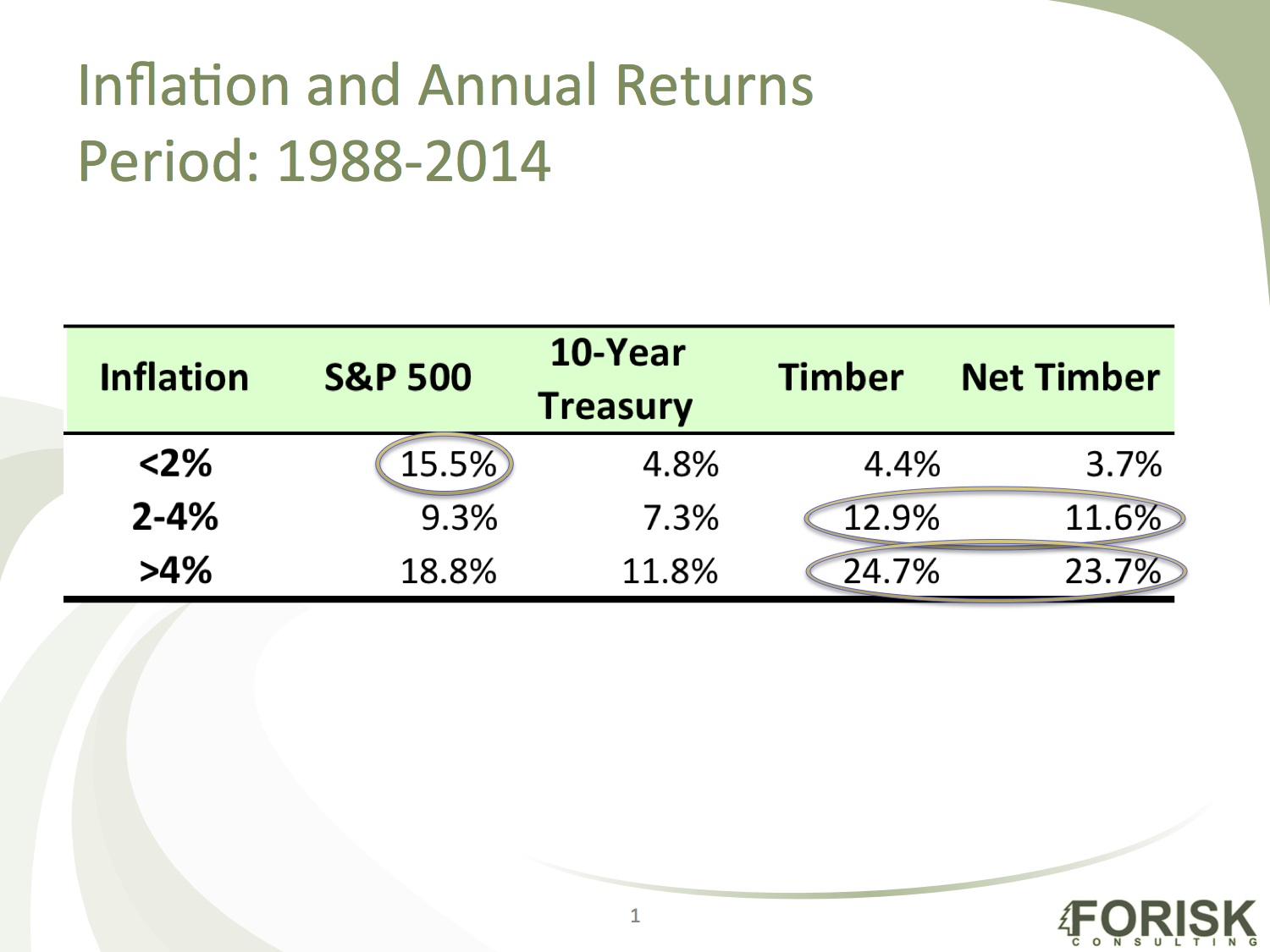

Fortunately, we can leverage readily available data sets to introduce timberland’s relative performance for specific questions. For example, one of the most common questions and attributes tagged to timber relates to its ability to hedge inflation. Given that inflation in the U.S. has been below 4% for 23 of the past 27 years (1988 through 2014), what have we learned on this topic?

To answer this question, we compare timberlands with investments in the S&P 500 (equities) and 10-Year U.S. Treasuries (bonds). For private timberland investments, we will apply annual data from the National Council of Real Estate Investment Fiduciaries (NCREIF), which publishes the most widely referenced index for the United States. The figure below highlights the relative performance of these three asset classes in different inflationary buckets. Overall, timberland outperformed the other assets on a relative basis in higher inflationary environments based on this data set. [“Net Timber” refers to estimated returns net of asset management fees.]

The concept of hedging inflation with timber deserves attention. Remember that inflation is an indicator of something else: prices, values, costs and returns are rising somewhere for someone; somebody makes money when inflation rises. So, if some seek timber to hedge rising inflation, does the corollary apply? Should we leave timber when inflation remains low? Ultimately, the relative performance confirms the academic literature, which finds that timberland performs well for hedging “unexpected” inflation.

Forisk will teach “Investing in Timberland and Timber REITs” in Atlanta on October 8h, a one-day course that details the operations, performance, risks and costs of available timberland investment vehicles.

Leave a Reply