The United Kingdom voted to leave the European Union and, as a result, David Cameron will step down as Prime Minister in October. The global implications of the British exit – “Brexit” – from the EU remain uncertain. It appears to complicate trade between the UK and member countries of the common market. If Scottish promises to vote on exiting the UK are realized, it also threatens the legacy of Sir Sean Connery as the greatest British spy.

What does Brexit imply for U.S. timberland investors and forest industry firms? Probably not much. Brexit implications concentrate on markets with strong exposure to wood pellets. Since U.S. wood pellet producers represent a small portion of the U.S. forest products industry, any impacts would be felt locally in key pulpwood markets, if at all. Even here, the risks reside within the context of increased uncertainty in three key areas: EU/UK energy policy, trade, and currency valuation (FX).

The main policy driving wood pellet demand is the EU’s implementation of its 2020 climate and energy package. It remains unclear if further policy changes will ensue with the exit or new political leadership following the resignation of PM David Cameron. The 2009 EU Renewable Energy Directive (RED), which is part of the energy and climate package, sets binding renewable energy targets for each EU member state. The RED set a target of 15% energy consumption from renewables by 2020 for the United Kingdom. Efforts to meet this target pushed biomass-based electricity generation from 3.8% of the national total in 2010 to 8.6% in 2015, with forecasts of 11% by 2020.

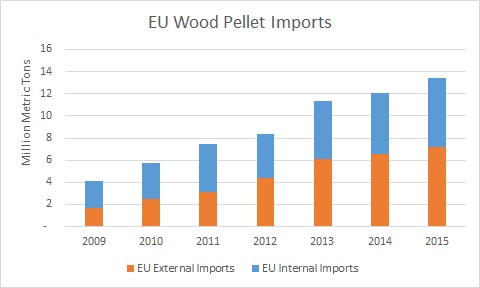

Source: Eurostat

As a result of the RED, Europe has become the world’s largest importer of wood pellets. The EU imported 13.5 million metric tons of wood pellets in 2015. Of these volumes, 7.2 million metric tons, 53.3%, were imported from outside the 28-country bloc and 6.3 million metric tons,46.7%, were imported from within (Figure 1). The UK represented 66%, 4.7 million metric tons, of these external volumes and 28.5% of the internal volumes. In 2015, the U.S. exported 3.8 million metric tons of wood pellets into the UK, which is 75% of all British non-EU wood pellet imports.

A UK departure from the EU would release the UK from the RED obligations, unless the UK maintains economic trade ties with the EU as part of the European Economic Area (EEA). An exit from the EU also releases the UK from compliance with EU State aid rules, which could simplify subsidy programs in the UK. The UK has developed its own climate change goals in the Climate Change Act of 2008 and has established programs to meet carbon reduction requirements, including the Contracts for Difference (CFD) program that provides subsidies for renewable energy technologies. Recent CFD budgets favor “less established technologies” such as offshore wind and biomass combined heat and power rather than biomass conversions, which have been driving the U.S. pellet export sector.

U.S. pellet manufacturers also face risks from volatility in the currency markets, as evidenced by the British Pound’s 8.1% drop in value. Most take-or-pay off-take contracts are dollar denominated, so U.K. firms importing U.S. wood pellets will pay more.

Finally, Brexit could tighten financing for unfinished projects if capital markets step back. Projects that plan to source wood pellets, such as Lynemouth and MGT, may face increased delays. Technically, nothing will formally change until the UK invokes Article 50 of Lisbon Treaty and begins the withdrawal process (a process that could take two years). In sum, the future of subsidy programs and funding efforts for renewable energy rest with Britain’s government and commitment as a country to continue supporting renewable energy and low carbon technologies, regardless the recent vote.

Andrew Copley, Amanda Lang and Shawn Baker supported the writing and research for this post.

The EU 2020 target is not the main driver in UK CO2 reduction policy, The Climate Change act of 1998 is. It sets 5yearly CO2 emissions budgets and UK is soon to enter the 4th budget period.

Probably biggest impact will be on investor confidence. European Investment Bank direct and with UK Green Investment Bank are big funders of Green Energy and EU utilities such as Dong Vattenfall and Norwegian Stadkraft are big investors in OffShore wind.