This is the third in a series related to the Q4 2018 Forisk Research Quarterly and Forisk’s annual “Wood Flows & Cash Flows” event on December 13thin Atlanta.

Sometimes you feel like a nut, and sometimes you don’t. Rising interest rates, slower housing, disruptive tariffs and trade policy, and the associated volatility in public markets produced a punishing quarter for public timber REIT values, while private timberlands held steady.

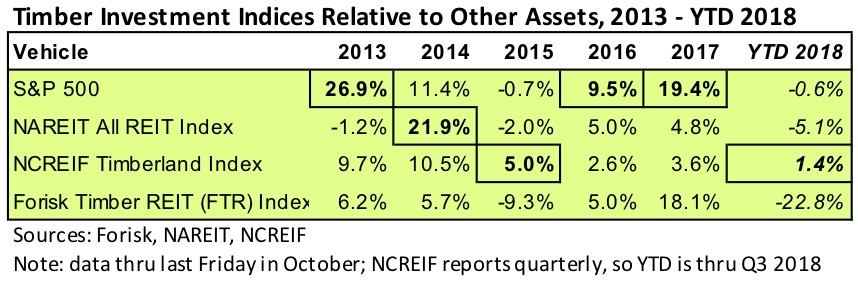

Public timber REITs returned -22.8% YTD through the last Friday of October 2018. Over the past twelve months, Rayonier (RYN), which currently comprises 15% of the timber REIT sector, led the sector with a 2.4% gain. Among public timberland-owning vehicles tracked in the FRQ, only Rayonier, among timber REITs, and master limited partnership (MLP) Pope Resources (ticker: POPE) netted positive stock price appreciation over the past twelve months.

The table below compares 2014 through 2017 annual and YTD 2018 performance of indices tracking the S&P 500, public real estate investment trusts (NAREIT), private timberlands (NCREIF), and public timber REITs (FTR). Timber REITs in the FTR Index include CatchMark Timber Trust (CTT), PotlatchDeltic (PCH), Rayonier, and Weyerhaeuser (WY). Year-by-year ranking highlights the shifting of capital and performance across investment vehicles, with the high volatility and periodic returns of equities (S&P, NAREIT and FTR) versus the relatively stable, positive returns of timberlands (NCREIF) since 2013. Timber REITs, which led YTD 2018 returns as of the previous quarter, are now on pace for their first negative year since 2015, which is also the last year private timberlands led this set of benchmarks.

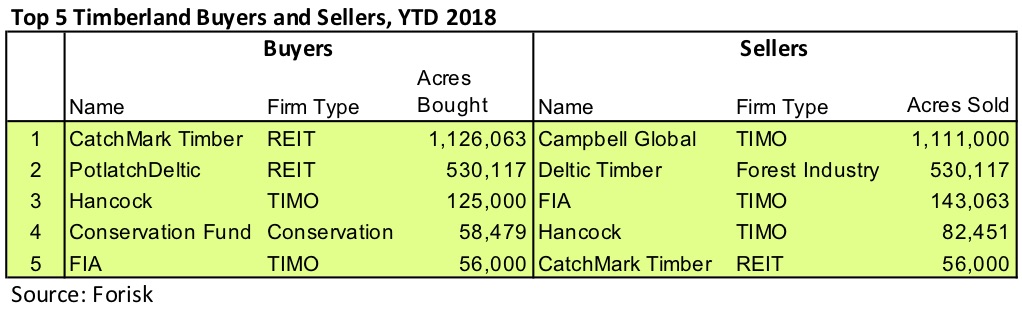

Since Q4 2017, nearly 2.6 million acres of institutional timberlands changed hands in the United States in deals exceeding 20,000 acres each. Over this same period, we tracked nearly 3.0 million acres of completed timberland transactions in the United States exceeding 1,000 acres in size (versus 3.3 million as of last quarter). TIMOs accounted for 62% of the total acres sold, while timber REITs accounted for 57% of total acres acquired. The table below includes the top 5 buyers and sellers of U.S. timberland year-to-date, with REITs leading on acquisitions and TIMOs leading on divestitures.

Interesting analysis, as always. Well done. One point to consider: With CatchMark’s recent acquisition of the former Temple Inland properties in Texas largely funded using institutional equity (~79%) in a structure that closely resembles a TIMO (including earning investment management fees and outsourcing all forest management to consulting firms), is it time to recharacterize CTT’s acquisition as that of a TIMO rather than a REIT? Hancock and Campbell are owned by Insurance companies, yet are classed as TIMOs rather than insurance companies. Food for thought…