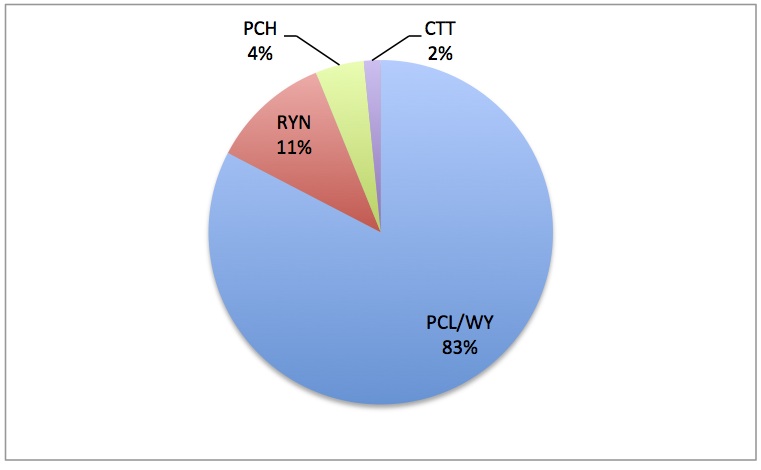

If the proposed merger of the two largest public timber REITs, Plum Creek (PCL) and Weyerhaeuser (WY), does anything, it reminds us of the relative insignificance of timber firms to the REIT sector generally and the stock market overall. Currently, the timber REIT sector includes five firms, with Rayonier (RYN), Potlatch (PCH) and CatchMark (CTT) rounding out the team. Prior to the merger announcement, WY comprised 55% of the sector’s market capitalization per the FTR Index. Following a merger, the enlarged WY would account for 83% of timber REIT market cap (Figure 1), likening the sector more to Saturn and its moons than a balanced set of firms. While each firm holds a diversified portfolio of timberlands, the sector itself would be condensed-milk concentrated.

Figure 1. Post Merger Market Capitalization of Timber REIT Sector by Firm, %

Data source: FTR Weekly Summary

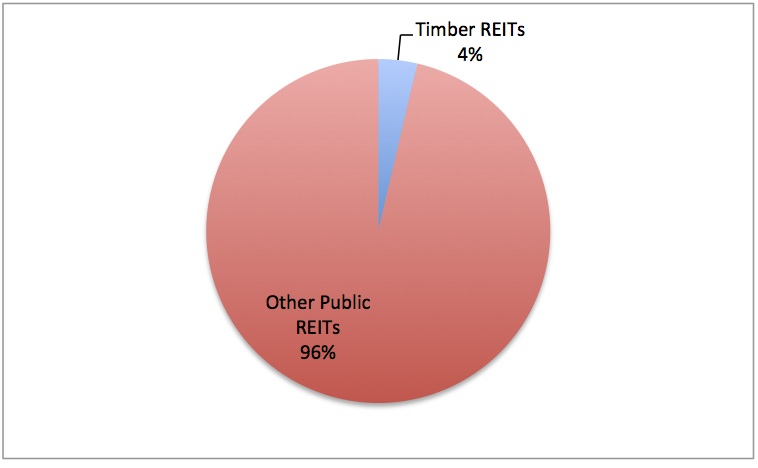

Scaling this group of timberland-owning firms to the public real estate (REIT) sector overall provides additional context (Figure 2). The five firms together comprise less than 4% of the total REIT sector’s ~$700 billion market cap. When we compare this to the $19+ trillion dollar market cap for the S&P 500, the merger looks quaint, like two brothers splashing around in one bathtub…of a house with nearly 1,000 bathrooms.

Figure 2. Timber REIT Market Capitalization Relative to All Public REITs

Data sources: FTR Weekly Summary, NAREIT

While the merger directly impacts employees of the two firms, the implications for timberland investors generally and wood-buying firms locally differ. Overall, a post-merger WY would still account for a small portion of private U.S. timberlands, and a fraction of the entire “investable universe” of industrial and institutional quality assets in the country (Figure 3).

Figure 3. Investable Universe Analysis for Timberlands in the U.S. (source: Forisk)

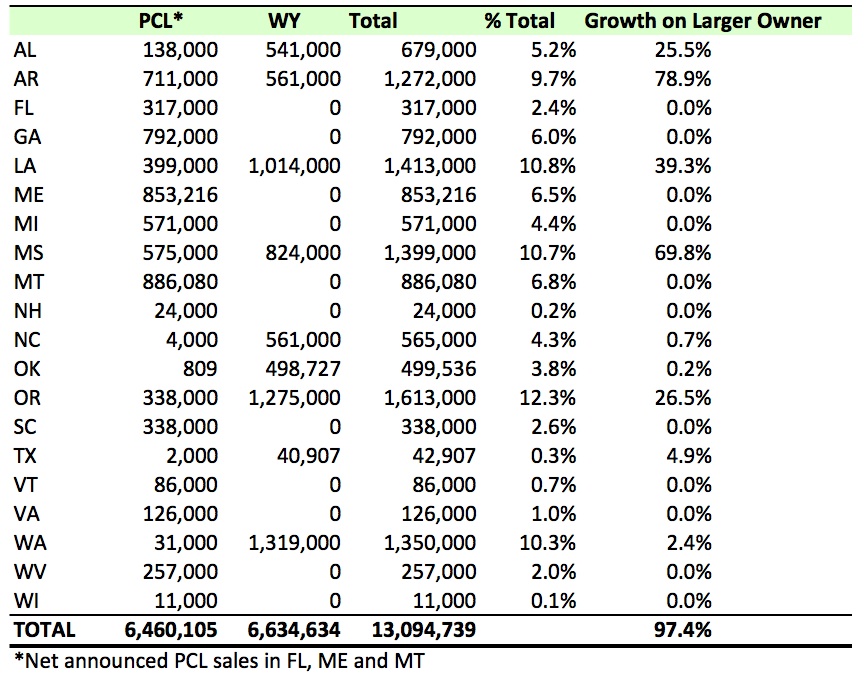

Localized timberland concentrations speak to questions of strategy and operational efficiency. The merger marries a portfolio heavy to the Pacific Northwest with another weighted to the U.S. South. Many “spatial” synergies exist. Of the 20 states involved, only five produce significant increases (25% or more) of owned timberlands (Figure 4). Strategically, the firms doubled down on the increasingly dominant role of the U.S. South in sourcing North America’s softwood lumber needs. Operationally, the lack of direct overlap “in the field” spotlights the reality that most synergies will flow from senior executives and centralized support services.

Figure 4. State Concentrations of Timberlands Owned by Post-Merger Weyerhaeuser

Source: Forisk Research Quarterly (FRQ)

For timberland investors generally, a key challenge remains evaluating and tracking the performance of their timber assets and managers. This is also difficult for the firms and forest managers themselves. As an inherently long-term investment, timberlands resist quarterly pigeonholing. However, as is the case with forest products manufacturers that can move production across a portfolio of mills as markets change, large timberland owners can shift harvests and resources across their timberland portfolios. But this is hard. With size comes risk and complexity. Saying it will happen and actually executing it remain two distinct challenges. And then, how do you know it actually happened?

For timber REIT investors, the analysis begins with tracking what can be measured publicly, and this starts with synergies. In addition, it increases the importance of tracking the smaller timber REITs and other timberland-owning firms, such as Deltic and Pope Resources. These firms become sources of sector-level insight by region that support efforts to track performance across timberland investment vehicles.

To learn more about the Forisk Research Quarterly (FRQ), click here or call Forisk at 770.725.8447. Featured research in the Q4 2015 FRQ outlines valuation approaches and estimated NAVs for the public timber REITs.

It is difficult to see that this merger creates value for WY shareholders.

The perpetuity value of the synergies relative to the value going PCL shareholders is marginally up-side down, utilizing a blended WACC. At best the merger may not materially change value; but the argument it creates value is difficult to see given the value of the synergies described. One wonders if the motivation for WY is tied to regulatory requirements for the non-reit taxable subsidiary.

Thank you for the comment. Yes, this point of view gets to the heart of the strategic thinking for the merger. At the end of the day, the timberland portfolio gets managed by individuals on the ground doing the best they can. With size comes complications associated with communications, tactics and coordination. Done well, exciting possibilities exist, but, as you note, the burden sits with the firms involved.