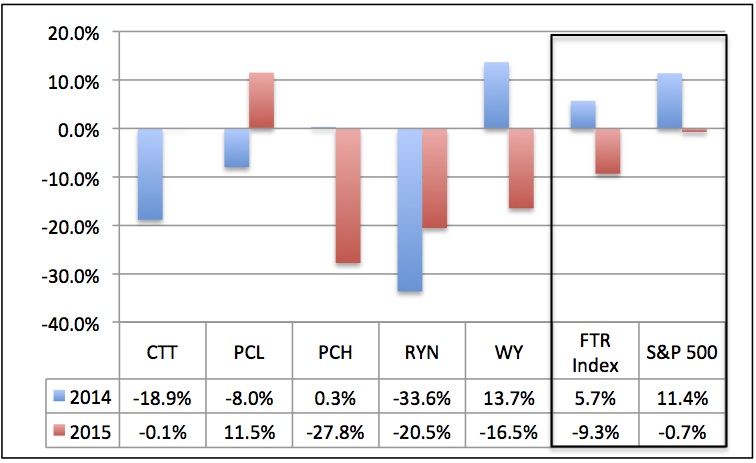

The timber REIT sector tumbled in 2015. The Forisk Timber REIT (FTR) Index fell -9.3% for the year, while the S&P 500 essentially flatlined at -0.7% over the same period. Of the five public timber REIT equities – CatchMark Timber (CTT); Plum Creek (PCL); Potlatch (PCH); Rayonier (RYN); and Weyerhaeuser (WY) – only Plum Creek generated positive returns for 2015 (Figure). And in the case of Plum Creek, its performance outpaced the sector only since its announced merger with Weyerhaeuser in early November.

Figure: Timber REIT Share Price Returns Relative to FTR Index and S&P 500, 2014 & 2015

Data source: FTR Weekly Summary

This marks the third consecutive year of timber REIT sector underperformance relative to the S&P 500. In 2014, the FTR Index returned 5.7%, simply because Weyerhaeuser, the only firm with meaningful positive stock price appreciation, accounted for 57% of the sector’s market capitalization. In 2013, timber REITs appreciated 6.3% as a sector relative to 29.6% for the S&P 500. However, four years ago, in 2012, the FTR Index returned 34.1% relative to 13.4% for the S&P 500.

History offers clues to timber REIT price moves. In 2012, the sector provided one method for betting on improved housing markets. Demand for shares increased along with modest recovery rates in housing starts and lumber. Increased capital investments in the U.S. forest products industry reinforced this thesis. Today, the physical facts on the ground with respect to forest industry capacity and growing demand continue to support this idea within the context of a cyclical business, and 2016 looks promising. The thesis requires time and remains exposed to the pace of housing, which sits firmly beyond management’s control.

That said, firm-specific activities also drive sector returns. The previously mentioned merger of Plum Creek and Weyerhaeuser, at a minimum, produced happy shareholders for one firm. [Between the day before the merger announcement and December 31, Plum Creek’s stock appreciated 18.4%.] In 2016, timber REIT performance outside of improved housing markets will largely rely on a successful WY/PCL merger, as the new entity will account for over 80% of the timber REIT sector. The analytic scorecard for management begins with tracking what can be measured publicly: merger milestones and synergy realizations. For industry analysts and investors, 2016 provides a case study for comparing large-scale private timberland investments with what could be possible with a fully formed, broad-based, publicly traded timberland portfolio.

To subscribe to the free weekly FTR Index Summary and to obtain historical FTR Index data in an Excel format, please sign up here or contact Heather Clark at hclark@forisk.com.

Leave a Reply