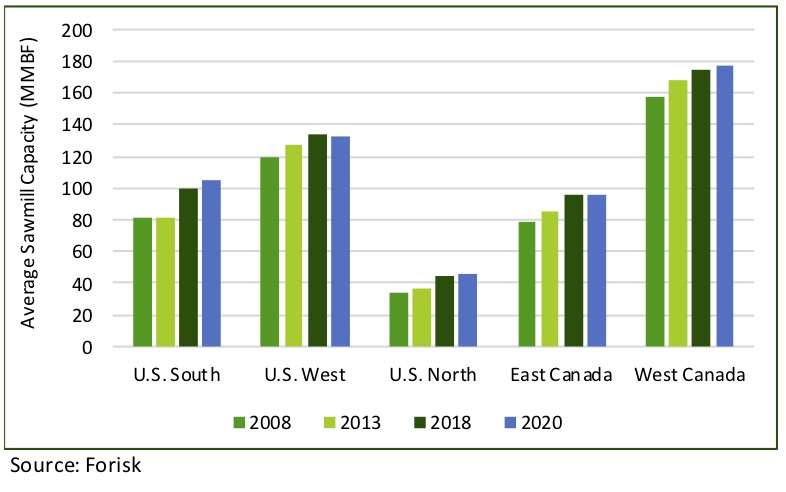

The nature and structure of sawmill capacity has changed over time. The figure below summarizes the average sawmill capacity by region since 2008 along with the expected profile of the industry through 2020. Between 2008 and 2018, while the number of sawmills decreased by 15% (from 761 to 647), the average softwood sawmill size increased 16% (from 96 to 112 MMBF). And the data indicates the recession accelerated this transition. While a number of regions have been expanding the capacity of existing mills, only in the South is capacity growth occurring through a meaningful increase of new sawmills, as well.

Figure: Average North American Sawmill Capacity by Region, 2008-2020

Note: sawmills <5 MMBF in annual capacity not included in the averages.

The growth of sawmill size corresponds with strategic decisions by individual firms: scale leverages technological advances in the forest products industry, and industry consolidation further leverages those benefits. The ten largest softwood lumber producers in North America have not changed much since 2008. West Fraser, Canfor and Weyerhaeuser still lead the industry, one-two-three (Georgia-Pacific sits at number five). However, over this time frame, the top ten went from 29.5 BBFT of capacity in 2008 (41% of North America’s total) to 34.0 BBFT in 2018 (48% of North American capacity). Coming out of the recession, the sector has also consolidated.

Data for this post comes from Forisk’s comprehensive analysis of North American wood-using capacity – current, historic and projected for 2008-2020 – by firm and sector across five North American regions. For more information, click, here.

Leave a Reply