This post introduces research covered in the Q1 2019 Forisk Research Quarterly (FRQ) and during the February 19th“Applied Forest Finance” course in Atlanta.

One reliable way to underperform as an investor is to buy into funds, stocks or assets at the top of the market. What gets priced up ultimately falls, adjusts or reverts to the mean thanks to arbitrage and rent-seeking capital flows. Alternately, outperformance thrives on the upside of undervalued securities, such as cash-generating hard asset businesses that lag the market. Recent history shows us that prime candidates from 2018 include publicly-traded, timberland-owning real estate investment trusts (TREITs).

What is the current situation with timber REITs? How could investors evaluate the opportunities in the timber REIT sector for 2019?

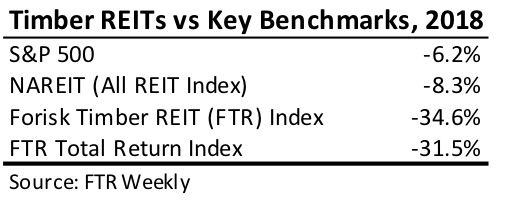

Timber REITs Tumble in 2018

Public timber REITs, along with the balance of the stock market, delivered truckloads of heartburn to investors, especially in the second half of 2018. For the year, the public timber REIT sector lagged far behind the S&P 500, which had its worst year in a decade. (In 2008, the S&P 500 returned -38.5% and the FTR Index returned -25.4%).

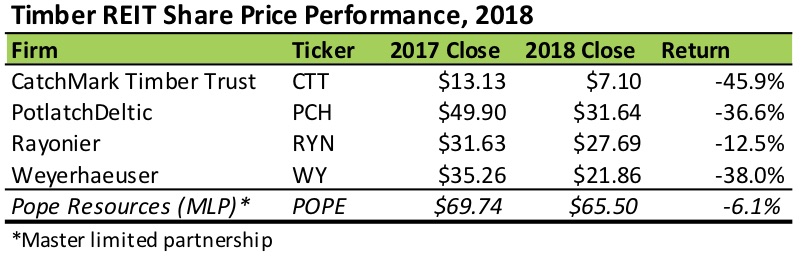

Even at the individual firm level, each stock underperformed the S&P 500. For comparison, timberland-owning Pope Resources, a master limited partnership (MLP), kept up with the broader market and outperformed timber REITs. (We note that the figures only reflect share (unit) price returns and do not include the distributions delivered by all five firms to their investors.)

Evaluating Timber REIT Investments

To track and evaluate the risk and potential returns of public timber REITs, we start with an ROV framework, applied in this order:

- Regulations: is the firm in danger of losing its REIT status with the IRS?

- Obligations: is the firm generating sufficient cash for key obligations? (Think “debt and dividends.”)

- Valuations: how are assets valued and performing relative to its current share price and over time?

The framework acts as a systematic screen that first addresses key regulatory and credit risks, followed by relative return potential and attractiveness. Investors value timber REITs when deciding whether or not to accumulate or dispose of shares. Does the firm’s share price imply that it’s under or over-valued relative to the value of its assets and future prospects? When valuing timberlands and timberland-owning REITs, estimating value is a function of estimating and, ultimately, discounting cash flows. If a timber REIT exhibits strengthened cash flows over time, this leads to expectations of higher distributions, high values and higher share prices.

While EBITDA multiples and liquidation analysis can be used for timber REITs, we employ several approaches for estimating and testing timberland values for assessing net asset values (NAVs). These include implied market values, regional index values, and localized asset analysis. Ultimately, investors attempt to identify timber REITs that are trading below estimated NAVs. The divergence between price and NAV could be a function of a lack of understanding of the properties, poor current market conditions or unattractive balance sheets. They could also reflect an over-reaction of the broader market. This is a key theme with respect to timber, as the longer-term prospects of a given firm are tied to longer-term cycles in housing, demographics and consumer goods.

The biggest risk for a potential investor is paying too much to get in. The biggest risk for a current investor is sub-optimizing the assets under management. As such, key metrics for evaluating timber REITs include net asset value (NAV), relative performance against private timberland investments and cash flows, both current and expected.

Click here to learn about and register for “Applied Forest Finance” on February 19thin Atlanta, Georgia. The course details necessary skills and common errors associated with the financial analysis of timberland and other forestry-related investments.

Leave a Reply