This post includes an excerpt from research published in the Q3 2017 Forisk Research Quarterly (FRQ).

Canadian forests support one of the world’s leading wood products industries. And that industry is in flux, rationalizing legacy investments in newsprint mills, navigating the forest supply repercussions of a massive beetle kill and periodic forest blazes, and (re)negotiating trade agreements with its largest trading partner. These challenges have led the industry to focus its efforts on investments and technologies that enhance its competitiveness into the future. These efforts include diversification of export markets and investments in wood-using technologies and product development to provide new growth opportunities for its forest products industry.

Globally, Canada maintains the largest forest product trade balance in the world. Most of Canada’s forest products trade balance results from outflows of value-added, manufactured products, not from exports of forest raw materials. While Canada produces over 11% of the world’s industrial roundwood, it consumes most of it domestically (as does the U.S.). Canadian log imports and exports tend to balance. Though exports exceeded imports the past six years, log imports exceeded exports for the 26 years before that back to 1984 (the year Canadian Alex Trebek first hosted the game show Jeopardy). Specific to the U.S., Canada is a net importer of logs, with most trade occurring between New England and Eastern Canada.

While Canada has the world’s third-largest forest base, privately owned forests account for only 6% of these acres. According to the Canadian Association of Forest Owners, woodlots owned by 450,000 families account for 80% of these private acres. Based on Forisk’s North American Timberland Owner Database, about two-dozen organizations – the largest of which include Domtar, J.D. Irving, TimberWest, Acadian and Island Timberlands – account for most of the balance.

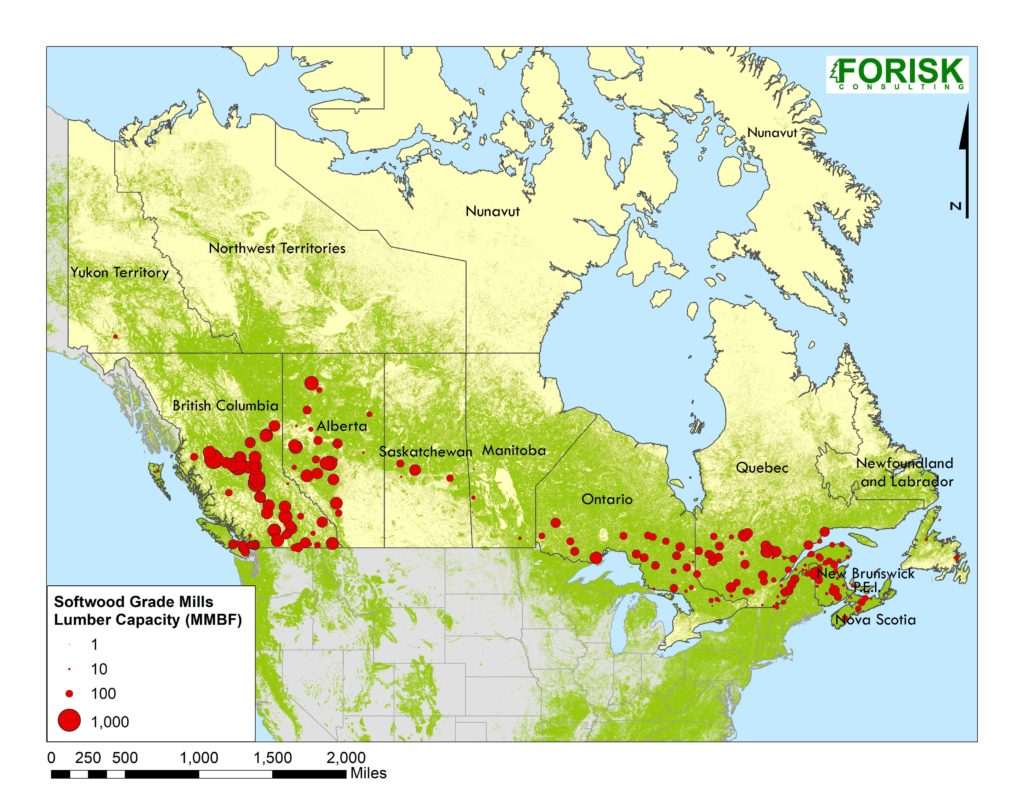

Interestingly, as in the United States, privately owned forests in Canada make a disproportionate contribution to national forest supplies. While accounting for 6% of ownership, private forests in Canada account for nearly 10% of harvested timber. Private forests are more common in Eastern Canada – which includes the provinces of New Brunswick, Nova Scotia, Ontario, Quebec – and British Columbia, which correspond to the location of the wood-using forest products industry (see map). The iron goes to the resource, especially when located near people and ports.

Data sources: Forisk Consulting, ESA GlobCover

This article profiles Canada’s lumber, structural panel, pulp and paper, and bioenergy sectors to provide context for its size, risks and strengths. The research supports Forisk’s forest industry scenarios and timber market models. To learn more, please click here or call Forisk at 770.725.8447.

Leave a Reply