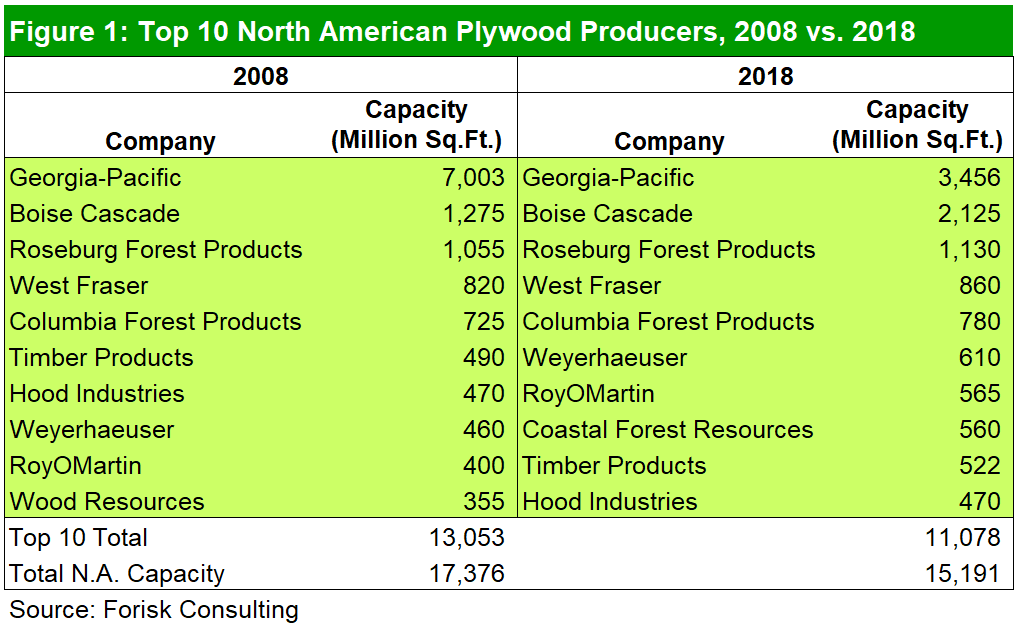

Structural panel production is highly consolidated amongst few firms in North America. There are only ten OSB producers and the ten largest plywood producers represent 73% of North American capacity in 2018.

The ten largest plywood producers in North America have not changed much since 2008. Georgia-Pacific, Boise Cascade, and Roseburg Forest Products still lead the industry, in that order (Figure 1). The dominant position Georgia-Pacific held in 2008 (39% of total capacity) has lessened, but GP still represents 22% of North American plywood capacity. Declining plywood capacity has not resulted in additional consolidation; the top ten firms accounted for 75% of capacity in 2008 and still account for 73% as of 2018.

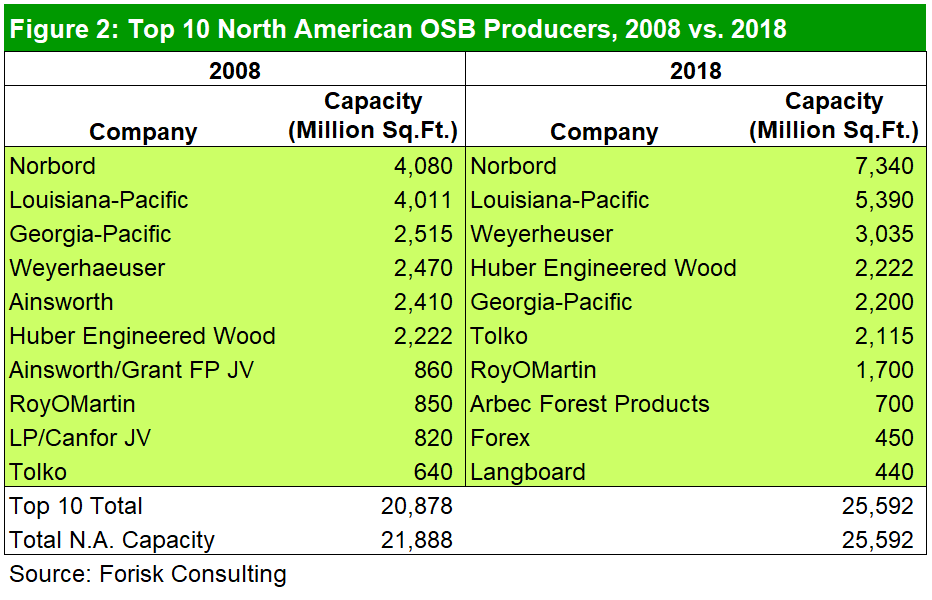

A discussion of the ten largest OSB producers in North America encompasses the entire industry (Figure 2). With total OSB capacity increasing 17% since 2008, the three largest firms each increased their capacity by 20% or more during this period. Norbord led the way with an 80% increase, further cementing their position as the top OSB producer in North America. Weyerhaeuser’s growth in OSB capacity pushed them from fourth to third on the list. The top three firms now represent 62% of OSB capacity, up from 48% in 2008.

This post contains an excerpt from Forisk’s Multi-Client Study: North American Forest Industry Capacity, a comprehensive analysis of wood-using capacity – current, historic and projected for 2008-2020 – by firm and sector across five North American regions. For more information, click, here.

Leave a Reply