This post introduces research and topics that will be addressed in the Q2 2024 Forisk Research Quarterly (FRQ), which includes forest industry analysis and timber price forecasts for North America.

Good questions clarify our context, risks, and options. Well-structured questions reveal new information and potential next steps. They help distinguish the important, relevant, and actionable from the unsubstantiated and uncontrollable. A quality question requires prioritizing issues and supports decision-making.

Three Types of Finance Questions

In forest finance, and in finance generally, three sets of questions organize efforts to screen and rank investments and potential capital projects:

- One, how do we identify, screen, and value timberland acquisitions or forest management decisions? These deal with the “investment decision” and includes proper valuation (appraisals) and the ranking of different forest management plans or timberland properties.

- Two, how do we pay for this investment? This is the “financing decision” and includes the relative advantages and disadvantages of using debt, cash, or equity.

- Three, how and when is the best time to sell a property, or to harvest timber? These questions comprise the “exit decision” and center on the timing of key activities.

To answer these questions, we apply specific discounted cash flow (DCF) tools to make the “best” investment decisions possible. These tools depend on two economic concepts from utility theory. One, we prefer more money rather than less. Two, we prefer dollars today rather than dollars tomorrow. These principles hold for everyone from kindergarteners to investment bankers; they help explain all basic financial criteria related to investing.

Criteria and Questions for Forest Investments

Most questions in forest finance flow from these economic concepts while tending to fall within the purview of the “investment” and “exit” decisions. Discounted cash flow (DCF) criteria – such as net present value (NPV), internal rate of return (IRR), and bare land value (BLV) – satisfy these economic principles through quantifying the time value of money and investor opportunity costs.

That said, my experience is that investment errors are less a function of misunderstanding economic theories and more associated with asking poorly defined questions, making unsupported assumptions, and missing simple spreadsheet errors. While we cannot control the state of the global economy and its impact on our investments and firms, there remain many things we can control when it comes to allocating capital, starting with how we define the key issue or question.

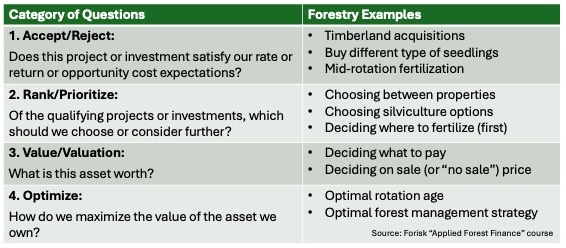

In forestry, we can organize fundamental investment questions into four categories, and each category addresses specific investment and operational issues:

Conclusion

When deciding where to allocate limited capital, we benefit by systematically applying available criteria for identifying, ranking, and optimizing the available options. Choosing which financial criterion to use depends on the question we’re asking.

For Part II, click here.

Leave a Reply