Introduction

Investors care about bond markets. For institutional investors tasked with managing portfolios on behalf of current and future retirees, U.S. policies and debt levels affect the relative attractiveness of assets from domestic timberlands to equities to treasuries. The bond market provides one way to assess the overall health of the U.S. economy.

Interest rates affect borrowing costs, capital investments, and home values. In forestry, specific fundamentals continue to favor the industry, including an aging and underbuilt housing stock (new homes needed!), and the renewability and sustainability benefits of wood products. However, the U.S. economy is dragging a piano while rounding the bases, delaying opportunities to get runs on the board[1]: U.S. federal debt is set to exceed $40 trillion dollars before November 2026.

Leon is Getting Larger

Currently, U.S. federal debt, growing at over $25 billion dollars per day, is about 22% bigger than the U.S. economy (U.S. debt-to-GDP ratio: 39.4/32.3 = 1.22). What does that mean? And why is it growing?

Using round numbers from the U.S. Debt Clock, the U.S. Government is spending just over $7.2 trillion and bringing in just under $5.6 trillion, producing a 2026 budget deficit of over $1.6 trillion. So far. To cover the gap, the U.S. Treasury issues securities to borrow money.

It is bizarre to think that, when we make car payments or mortgage payments on our homes, our family debts shrink, and yet the U.S. government debt grows. The reason, like it or not, is that the government continuously “rolls over” the debt, issuing new securities to pay off the old bonds as they mature (which feels frightfully Ponzi-like to me, but I’m simply an unfrozen forest analyst).

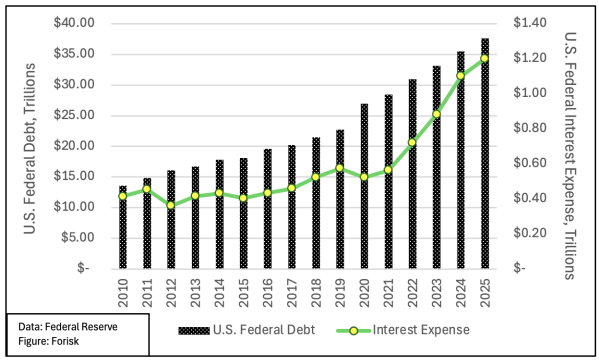

The repercussions, however, reveal themselves in the interest payments made to finance and refinance the debt (figure). Since 2010, the U.S. debt has tripled in size. In 2024 and 2025, the government spent over $1 trillion in interest and has already spent in excess of $1.1 trillion in 2026, with months to go.

Data Source: U.S. Federal Reserve

U.S. Treasury Refresher

How does this financing work? What are the implications to investors generally and, in my world, the forest industry? When investors buy bonds, they effectively lend money to the government. These “loans” comprise IOUs from the U.S. government, accounting for a large share of the national debt.

Treasury yields refer to the total amount of money you earn on these instruments — bills (less than 1-year terms), notes (2-to-10-year terms) or bonds (longer than 10-year terms) – sold by the U.S. Treasury Department to finance the debt. Remember: Treasury yields fall when demand increases for Treasuries, which investors view(ed) as ‘safe’ investments. As with timberlands, when prices go up, expected returns on capital invested go down.

From a lender’s perspective, the most critical aspect of underwriting a loan is the cash flow analysis. This should also be the most important consideration for a borrower. As I note in Forest Finance Simplified, when it comes to using leverage for timberland investments or any other asset, the question is, “Can the investment – and investor – service the debt and pay the bills?” This also affects the view of investors in U.S. debt.

Bond Market Realities Reinforced

In sum, the bond market is the primary mechanism for financing the U.S. national debt. When demand for U.S. bonds rise, the prices of those bonds also rise, and their yields fall. That means investors are satisfied with lower interest payments and the U.S. government enjoys cheaper borrowing costs.

However, when demand for U.S. bonds fall, the prices of those bonds also fall, and their yields rise. That means investors require higher interest rates to “lend” the government money, and government borrowing costs increase, as a result. When might this happen? When investors get nervous about economic growth, political instability, liquidity, and the general health of the patient, they ultimately require higher yields to compensate for growing perceived risks.

At the end of the day, bond markets care about (1) the timely payment of interest and repayment of principal, and (2) the value eroding effects of inflation on these investments.

Conclusion

The forest industry and timberland investors have broad exposure to the overall health of the U.S. economy, as measured through growth, housing markets, aggregate demand, and the cost of borrowing. The U.S. national debt, the annual spending deficit, and the interest expense associated with financing this exercise are key signals associated with tracking the health and resilience of the economy. In the end, it is the bond market that serves both to facilitate and, when worried, constrain the flow.

To learn more about the Forisk Research Quarterly or Custom Market Forecasts, contact Nick DiLuzio (ndiluzio@forisk.com).

#

[1] My humble effort to mix a few metaphors.

Leave a Reply