“The best time to plant a tree was 20 years ago. The second best time is now”

This proverb, often attributed to China, encourages action today even if you failed to act earlier. It also echoes a fundamental truth, and challenge, of forestry: the forest we have today is a product of past actions. Trees take time to grow and those lags make balancing timber supply and timber demand challenging. Anyone who’s had the pleasure of playing MIT’s management simulation “The Beer Game” knows that even short delays between supply and demand can cause huge surpluses and shortages.

A similar dynamic could now occur across the U.S. South as the wood pulp industry contracts and pulpwood demand declines. Landowners are rethinking their planting density (how many trees they plant per acre) to lower the risk of being “forced” to thin a stand when few or no markets are available for the harvested trees. With lower current demand there is a surplus of pulpwood supply and landowners are responding.

Historic Planting Trend Impacts

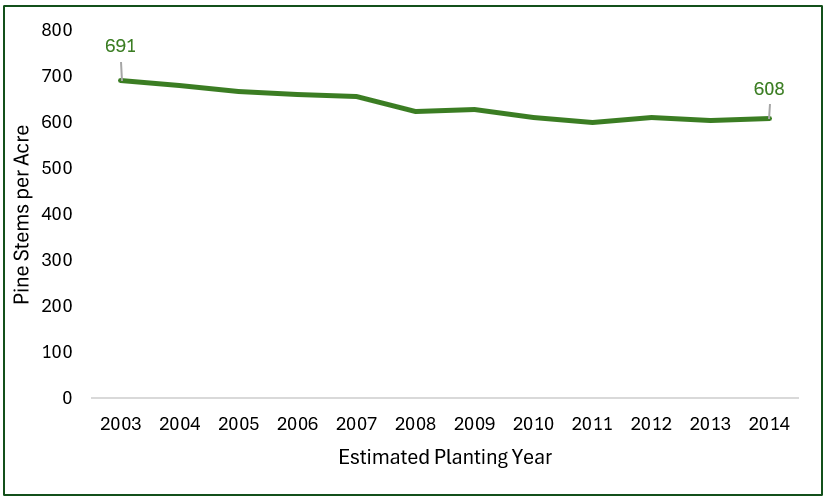

The trend toward fewer trees per acre is not new. Historic data from the US Forest Service Forest Inventory and Analysis (FIA) program shows the long-term decline in planted southern pine pre-thinning stems per acre on private timberlands (Figure 1).

FIA data is backward-looking due to measurement and reporting lags. The most recent FIA data available south-wide is the 2024 panel which draws on measurements collected over the previous five years and roughly represents a 2022 inventory. That means in the most recent data, stands aged 6 to 10 years average about 8 years old and were initially planted around 2014 (a midpoint estimate). The stand density in this age class declined over the past decade. Average stocking of these young pine stands dropped from 690 stems per acre for stands planted in the early 2000s to under 610 in the most recent inventory.

Where Are We Headed Next

With the long timeframes of forestry, it can be difficult to predict where trends are headed. Forisk’s southern silviculture surveys track management practices of large timberland owners and managers. Our data shows these large landowners continued the downward trend, planting 90 fewer trees per acre in 2025 than in our initial 2012 survey. The surveys provide a leading indicator that stem counts on thinning-age stands will likely be declining for another decade (at least!).

With pulpwood prices and demand down substantially across the South, landowners are responding rationally to the current market. Most observers agree that the majority of closed pulp mills are unlikely to reopen. Still, no one knows how markets will develop over the next 15 years and if we will see new demand for pulpwood among emerging technologies. Lower planting densities help landowners avoid thinning, but they also cement the future timber supply in ways that may matter if fiber demand strengthens. As landowners across markets look at dense pine stands that need thinning with few markets to take their trees, many may be wondering whether the best time not to plant a tree may have already passed.

Forisk’s Western Silviculture Survey is currently underway. If you would like to participate, please reach out to Shawn Baker at sbaker@forisk.com. For information on Forisk’s full offering of forest industry research and analysis, contact Nick DiLuzio (ndiluzio@forisk.com)

Leave a Reply