This post includes excerpts from the Q2 2026 Forisk Research Quarterly (FRQ), which includes forest industry analysis and timber price forecasts for North America. To learn more or to subscribe to the FRQ, please contact Nick DiLuzio (ndiluzio@forisk.com).

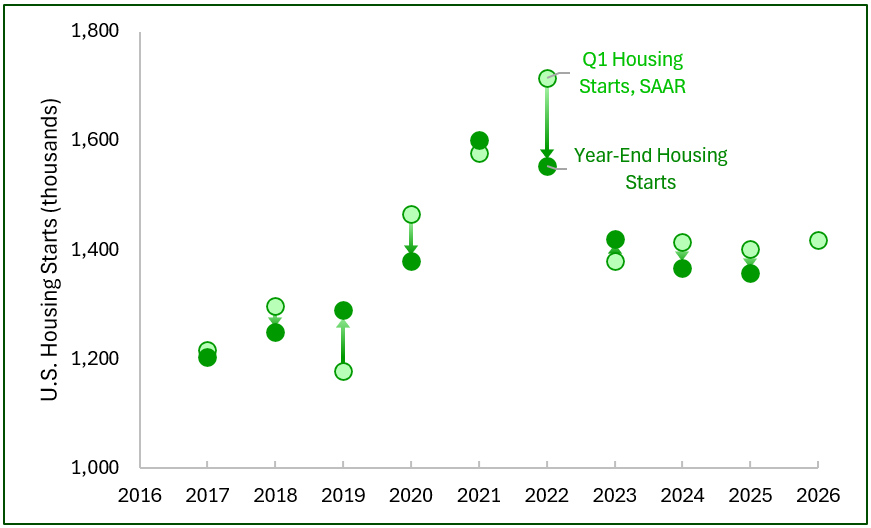

Year-to-Date Housing Activity

Seasonally adjusted annual rates (SAAR) for U.S. housing starts averaged 1.42 million in Q1, up 7.2% from Q4’s 1.32 million SAAR. Single family starts rose 3.5% to 957 thousand SAAR while multifamily starts jumped 16%. Building permit activity was less dynamic, with Q1 2026 permits flat relative to Q1 2025 and up 1% from last quarter. New home sales were down 5% year-over year.

The pace of Q1 housing starts was a welcome sign of good news, particularly given the significant increase in March (surpassing 1.5 million starts on a seasonally-adjusted basis), marking the highest Q1 start level since 2022. Historically, Q1 has not been a perfect indicator of full-year housing activity. Over the last nine years, the Q1 housing start SAAR averaged around 25 thousand more starts than ultimately occurred by year-end (Figure 1). In six of the last nine years, the Q1 SAAR was within 50 thousand starts (~4%) of year-end actuals. In three years (2019, 2022, and 2025), the direction of change from the previous year’s actual starts to the subsequent Q1 rate differed from the year-end to year-end direction of change. The Q1 2026 housing start rate is similar to the pace each of the last three first quarters, despite a slow decline in year-end activity.

Data Source: U.S. Census Bureau

Methodology

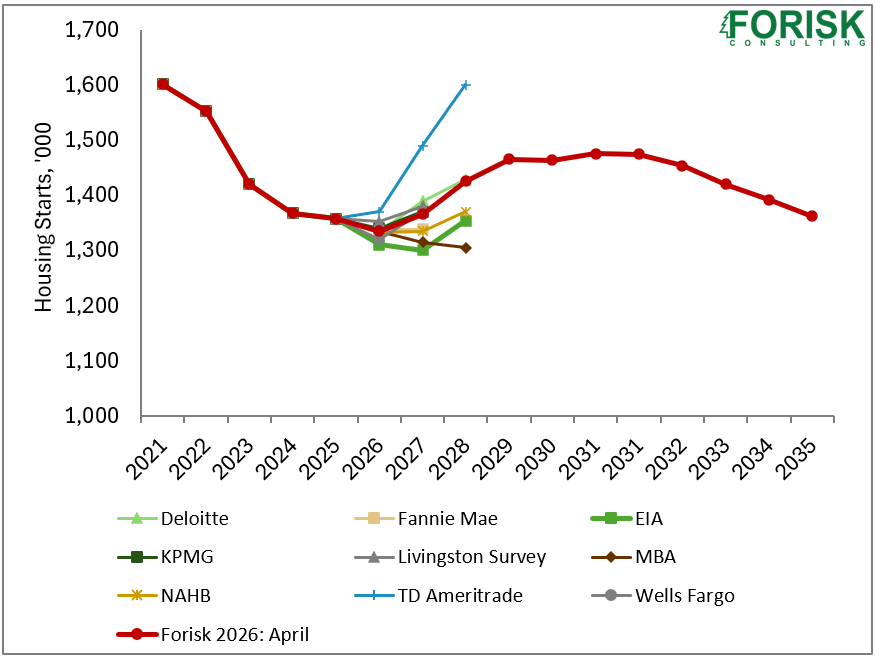

Each quarter when updating our Forisk Research Quarterly (FRQ) forecast models, we revisit prior projections and review applied research on the economy. Forisk’s Housing Starts Outlook combines independent forecasts from professionals in the housing industry. Currently, these include Deloitte, Fannie Mae, the U.S. Energy Information Administration (EIA), KPMG, the Livingston Survey, the Mortgage Bankers Association (MBA), the National Association of Home Builders (NAHB), TD Ameritrade, and Wells Fargo. Forisk applies long-term assumptions from the U.S. Energy Information Administration (EIA) and Harvard’s Joint Center for Housing Studies to establish the peak and trend over the next ten years.

Near-term Housing Outlook

Housing starts totaled 1.36 million units in 2025. We project a 1.5% decline to 1.34 million units in 2026, followed by a recovery to 1.37 million units in 2027 (Figure 2). The outlook for 2027 housing starts is consistent with our Q1 2026 forecast, but 100 thousand starts fewer (-7%) than our outlook one year ago. Among published Q1 housing forecasts compiled to calculate our consensus outlook, even the most bullish only anticipated a 1% increase in 2026, with the remainder anticipating a 1-3% decline. Forecasts for 2027 were more mixed, with half anticipating housing start increases from 2026-2027 and the remainder anticipating either flat or declining starts.

Data Sources: Deloitte, EIA, Fannie Mae, KPMG, Livingston Survey, Mortgage Bankers Association (MBA), National Association of Home Builders (NAHB), TD Ameritrade, Wells Fargo.

Leave a Reply