This post is an excerpt from the Q2 2026 Forisk Wood Fiber Review (WFR), which provides a quarterly review of pulpwood, chips, biomass markets and trade in the U.S. and Canada.

Introduction

Residual wood chips, byproducts generated during timber harvesting (whole-log chips) and milling operations (mill residual chips), are vital to the forest products industry. They provide secondary revenue streams for landowners and mills, offset landfill waste, and serve as raw materials for pulp & paper and renewable bioenergy.

PNW Market Impacts

Pacific Northwest chip markets experienced significant changes over the last several quarters. The closure of Domtar’s paper mill in Crofton, BC decreased the demand for barged chips from the PNW. Packaging Corporation of America’s (PCA) Wallula, WA mill also stopped purchasing virgin wood fiber, further decreasing chip demand. In Q2 2026, Weyerhaeuser avoided a potential strike, International Paper purchased North Pacific Paper (NORPAC) from One Rock Capital Partners, and Nippon Dynawave Packaging in Longview, WA experienced a tragic chemical tank explosion with 11 fatalities. While impacts from these events continue to unfold, Q2 saw decreased demand and fiber pricing. Most buyers and sellers reported moving lower volumes as they used existing inventories to avoid high transportation costs. Whole-log chip producers, often the most expensive option, were “cut” first by many buyers.

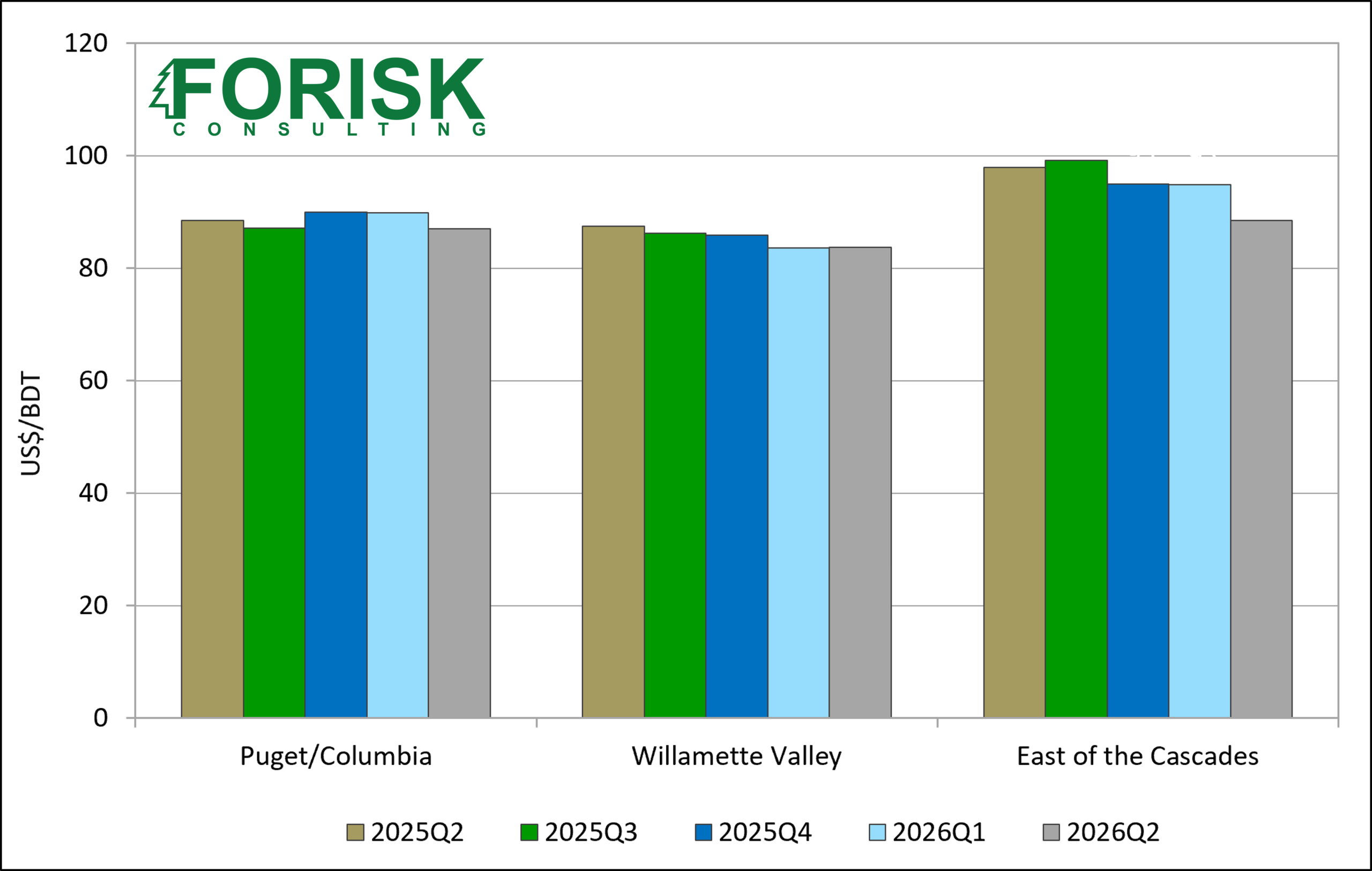

Second Quarter Pricing

The Q2 PNW weighted-average price for combined residual and whole-log softwood chips was $86/BDT. Puget/Columbia prices (residual and whole-log softwood, including pine) were down 3% from Q1 and Willamette Valley prices were flat. East of Cascades prices were down 7% due to increased supply, partially due to PCA’s Wallula facility no longer purchasing chips. PNW Douglas-fir and hemlock (residual and whole-log) were down 3% and 4% respectively. Regional decreases in delivered pricing occurred in spite of increased fuel costs for buyers and sellers.

Data Source: Forisk Wood Fiber Review

*Prices are weighted average of residual and whole log chips

Leave a Reply